Global Economy Expanded More Slowly than Expected in 2011

The global economy grew 3.8 percent in 2011, a drop from 5.2 percent in 2010. Economists had anticipated a slowdown, but this was even less growth than expected, thanks to the earthquake and tsunami in Japan, unrest in oil-producing countries, the debt crisis in Europe, and a stagnating recovery in the United States. As richer economies struggle to recover from the financial crisis of 2008–09, poorer countries are facing high food prices and rising youth unemployment. Meanwhile, growing income inequality and environmental disruption are challenging conventional notions of economic health.

|

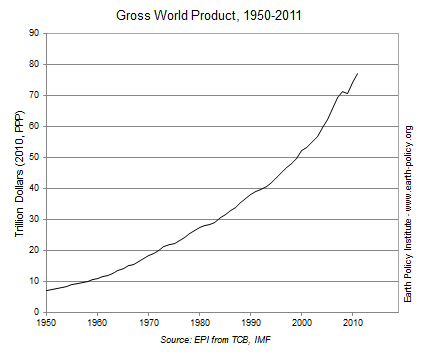

The total value of goods and services produced worldwide in 2011 was $77.2 trillion, twice as much as 20 years ago. The global economy expanded by an average of 4 percent each year in the decade leading up to the 2008 slowdown and the 2009 contraction. Industrial economies typically grew by about 3 percent annually in the 10 years before the recession but only 1.6 percent in 2011. Developing economies, which grew by an average of roughly 6 percent annually in the decade before the recession, grew by 6.2 percent last year.

Developing Asia was responsible for 25 percent of global economic output in 2011. China’s economy, the world’s second largest, grew 9.2 percent in 2011, producing $11.1 trillion in goods and services. Yet this was a much slower expansion than its pre-recession rate of 14 percent in 2007. India, whose gross domestic product (GDP) grew by 7.4 percent to $4.4 trillion in 2011, surpassed Japan to become the world’s third largest economy. (See data.)

The 2011 growth in developing Asian economies was dampened somewhat by the disaster in Japan, which disrupted global supply chains in automotives, electronics, and other sectors. Japan’s economy also took a hit, contracting by 0.9 percent to $4.3 trillion in 2011. More